Posted on: 9th July 2020 in Retirement Planning

Covid-19 has caused chaos in every part of our lives.

The way we work, shop and socialise have all been affected. Even people’s retirement plans are up in the air.

Millions of workers have seen their retirement plans disrupted, and in some cases, completely derailed.

So, how has Covid-19 had such a severe effect on retirement plans? Generally speaking, there are two factors.

Firstly, the pandemic has led to widespread job losses. With incomes compromised, people may be unable to stay on track with their savings goals.

The second issue is the market uncertainty caused by Covid-19, which has hurt pension pots.

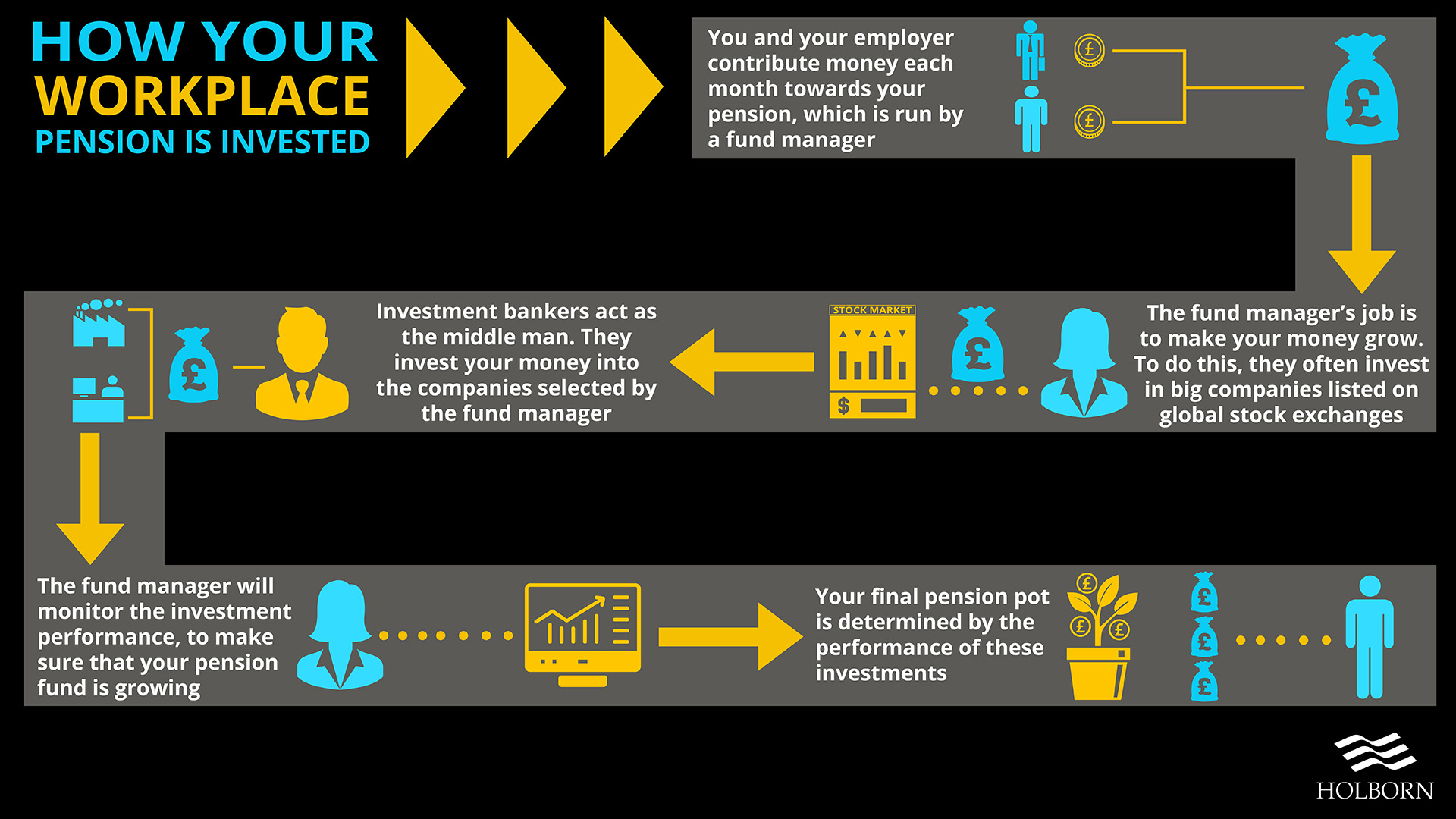

Most people will have a defined contribution pension, either in the form of a personal or workplace pension.

Whether you have a personal pension or a workplace pension, they both rely on one thing – market performance.

To understand why pension pots have suffered, let’s take a look at how they are invested. Here is a general overview of the journey your money takes with a workplace pension.

The financial performance of companies has suffered as a direct result of the pandemic. Remember, your pension ultimately relies on the performance of investments in these companies.

Not only have market fluctuations affected pension pots, but contributions are also lower.

Millions of furloughed workers saw their salary drop by 20% as the government pledged to cover 80% of wages up to £2,500 a month. Pension contributions during the furlough period are likely to be based on four-fifths of your salary.

When it comes to assessing the damage that the pandemic has caused to retirement plans, the numbers speak for themselves.

Research by financial service company Aegon found that 18% plan to delay their retirement as a result of Covid-19. Things are also looking bleak for those who work for themselves.

40% of self-employed workers said they are reassessing their retirement plans, with 22% planning to delay their retirement.

Having enough saved for retirement was already a concern for millennials. Before the pandemic, research by YouGov found that 58% of millennials were worried that they would not be able to support themselves financially in retirement.

Younger workers from the millennial and Gen Z cohorts are decades away from retirement. Still, it seems they have been affected by the chaos caused by Covid-19.

Aegon revealed that 21% of those aged 18-34 expect to delay their retirement. While there is a worry for younger members of the workforce, there is a growing concern for those nearing retirement.

According to data from the Office for National Statistics (ONS), there are 1.42 million workers over the age of 65.

The figures represent a record high, and the ageing workforce looks set to grow as a direct result of Covid-19.

A separate report by Legal & General revealed that 1.5 million workers over the age of 50 could be forced to delay retirement. Of those, 15% said they would delay retirement by three years, and 26% said they expect to work indefinitely.

All of this may seem negative, but don’t panic! It’s clear that Covid-19 has hit retirement savings, but there are signs of improvement.

The markets are slowly returning to normal and beginning to stabilise. As a result, defined contribution pensions are starting to recover.

Remember, pensions are just like any other investments. They are usually a long-term way to build wealth.

Younger workers have time on their side. Thanks to compounding returns, most will be able to get their pension pot back to pre-pandemic levels.

Those nearing retirement may not have time to recover losses, but their pensions could be more protected.

Part of a defined contribution pension will also be invested in bonds. Bonds are considered a safe investment and have a much lower risk than shares. Not only are bonds low risk, but they also offer a fixed rate of return.

As you get closer to retirement, workplace pensions tend to invest in these low-risk assets.

Most workplace pensions have a dashboard which allows you to see where your money is invested and how it is performing. Before making any hasty decisions, it’s worth checking the status of your pension.

Planning for retirement can be a challenge at the best of times. In the current climate, there are even more things to consider. With the right strategies in place, it is still possible to keep your retirement plans on track.

If you are concerned about your retirement, speaking with a financial adviser can help. To talk to one of our experts and find out how we can help you, contact us using the form below.

We have 18 offices across the globe and we manage over $2billion for our 20,000+ clients

Get started

As an expat, navigating the world of taxes can feel like wandering through a maze. Different countries have their own rules and regulations, making it easy to get lost in...

Read more

Retirement planning can be a daunting task for anyone. For expats, the process can seem even more complex. Whether you’ve spent years living and working abroad or are planning to...

Read more

Navigating the world of investments can be tricky for anyone, but expats face unique challenges that can complicate the process even further. Whether you’re settling into a new country or...

Read more

The closing ceremony at the Stade de France brought the curtain down on the 2024 Olympics. While the Games may be over, their impact on the host city’s property market...

Read more