Posted on: 28th July 2020 in Mortgage & Property

If you were considering investing in UK property, now might be a perfect time.

Recent changes to stamp duty made by the government could save investors thousands of pounds.

Let’s start by taking a look at what stamp duty is and what has changed.

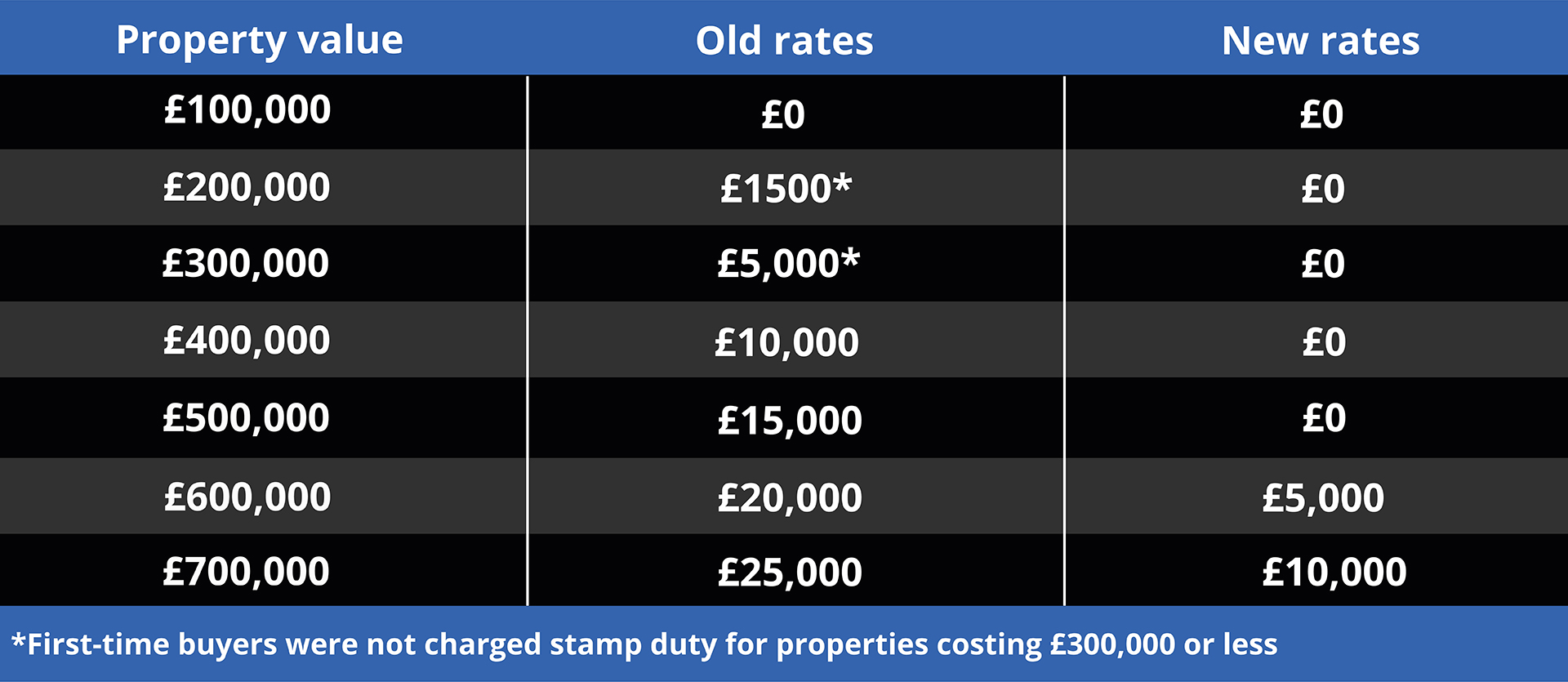

Stamp duty is a tax that you pay when you buy a property in England or Northern Ireland.

Under normal circumstances, you will pay stamp duty if the property is over £125,000. The amount of Stamp Duty Tax that you pay will depend on the purchase price of the property. The more expensive the property, the more you will pay in stamp duty.

For first-time buyers, it’s a little different. If you are buying your first home, you won’t pay stamp duty on a property costing £300,000 or less.

However, this has all changed as of 8 July 2020.

In a bid to boost the UK property market, the government has increased the stamp duty threshold – but it’s only temporary .

Between 8 July 2020 and 31 March 2021, buyers won’t pay stamp duty on properties costing 500,000 or less.

The changes not only apply to first-time buyers, but they also extend those who have previously owned a property.

Under the new rules, buyers could save up to £15,000.

The stamp duty holiday will no doubt help buyers who have taken a financial hit during the pandemic. However, things work a little different for those purchasing a home that will not be their primary residence.

So, what do the changes mean for investors who might be interested in a buy-to-let property?

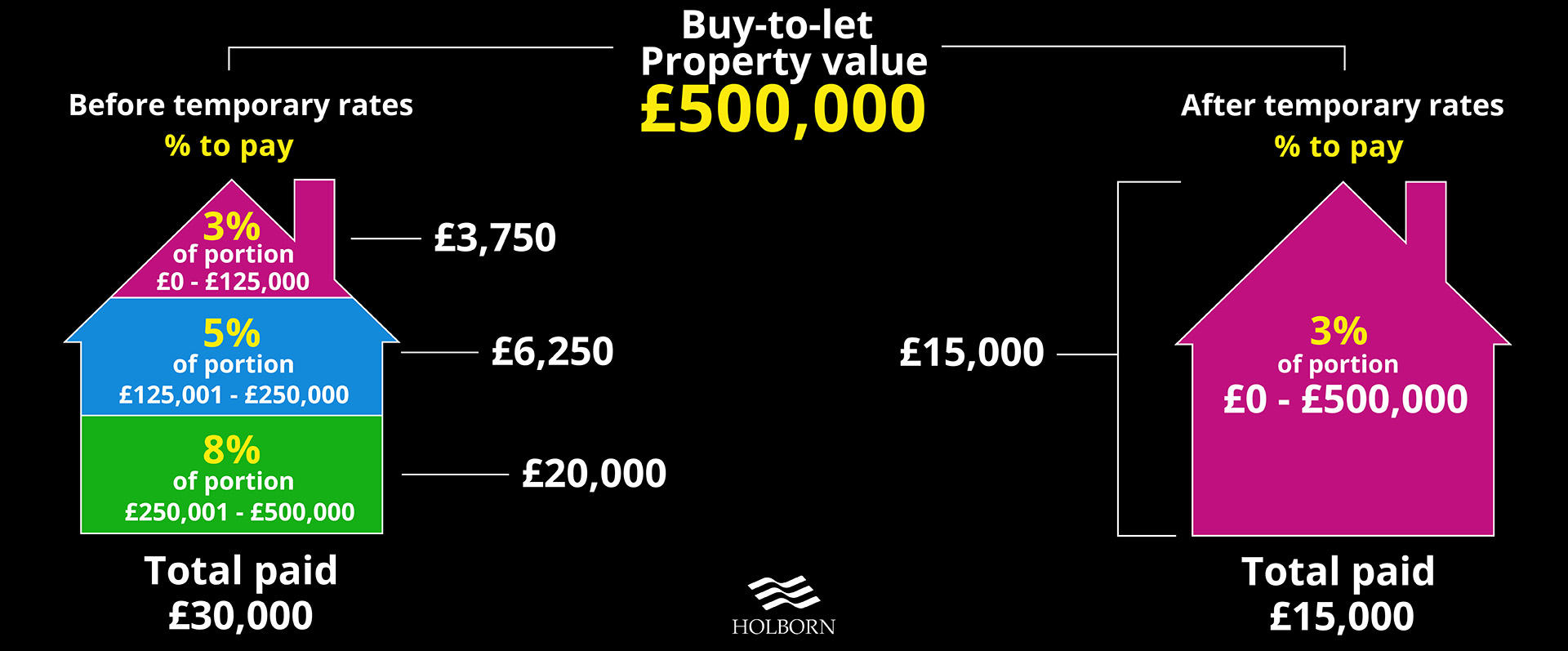

On top of regular stamp duty, buy-to-let properties are subject to an additional surcharge.

Properties are broken up into bands, or portions. Each portion is subject to an increasing surcharge percentage.

Here is how the stamp duty surcharge worked before the temporary rates.

Despite the additional costs, investors could now save thousands of pounds. That’s because the stamp duty surcharge is based on the new temporary rates.

Here is how the stamp duty surcharge will work under the temporary rates.

To make sense of this, here is the total cost of a £500,000 property before and after the temporary rates.

Use our calculator to work out how much stamp duty you would pay on a buy-to-let property before and after the temporary rates.

The property market hasn’t been immune to the effects of Covid-19.

In June, Nationwide reported that house prices were 0.1% lower than the previous year – the first annual fall in eight years.

The building society also revealed that house prices dropped by 1.7% and 1.4% for May and June respectively. The figures represent the biggest monthly declines since the financial crisis. Although, comparing the current climate to that of 2008 might not be a fair comparison.

The financial crisis was directly related to the banks. Because of this, mortgages were harder to come by, and interest rates were less favourable. The opposite could be said about the current state of the property market.

In response to the pandemic, the Bank of England has reduced its base rate to 0.1% . Unlike the events that followed in 2008, banks are lending at favourable rates, which is great news for investors.

So, if we are being encouraged to buy with government incentives and good loan rates, what has caused the recent dip in property value?

The impact on the housing market seems to be linked to a lack of activity, and figures could back up this theory.

Lockdown measures have begun to ease across the UK. People are now able to view properties and visit banks, which has led to a spike in interest.

According to Rightmove, the increased activity in the market has led to an increase in house prices.

The property portal found that average asking prices have increased by 2.4% since before the lockdown. The annual pace of growth is also up by 3.7% – the highest it has been since December 2016.

No investment is a sure thing. However, property has proven to be resilient.

Historically, the property market has stabilised and come back stronger, no matter what was thrown at it.

For investors looking to diversify their portfolios , property remains a viable option, despite recent dips.

To find out more, you can contact one of our property experts by using the form below.

We have 18 offices across the globe and we manage over $2billion for our 20,000+ clients

Get started

As an expat, navigating the world of taxes can feel like wandering through a maze. Different countries have their own rules and regulations, making it easy to get lost in...

Read more

Retirement planning can be a daunting task for anyone. For expats, the process can seem even more complex. Whether you’ve spent years living and working abroad or are planning to...

Read more

Navigating the world of investments can be tricky for anyone, but expats face unique challenges that can complicate the process even further. Whether you’re settling into a new country or...

Read more

The closing ceremony at the Stade de France brought the curtain down on the 2024 Olympics. While the Games may be over, their impact on the host city’s property market...

Read more