A practical guide to Estate Planning

This practical guide to estate planning explains why it matters, how to protect your assets, minimise tax and plan for the future.

Estate planning is more than just writing a will—it’s about having a solid plan in place that ensures your loved ones are protected, your wealth is preserved, and your wishes are respected.

Whether you have a modest estate or complex global assets, having a clear, legally sound plan ensures that what matters most to you is handled in line with your wishes.

This guide breaks down the fundamentals of estate planning. We will cover why it matters, the key estate planning tools and how to begin creating a plan.

Estate Planning: The Key Points

- It is the process of legally organising how your assets are distributed

- A solid estate plan can include wills, trusts and powers of attorney

- Proper planning can help reduce taxes, avoid probate and protect your loved ones

- An estate plan can be tailored to those with special requirements, such as expats and high-net-worth individuals (HNWIs)

- Common mistakes include not updating your plan and ignoring digital or cross-border assets

What is Estate Planning?

Also known as legacy planning, estate planning involves deciding how your assets will be managed and distributed after your death. It can help you prepare for the unexpected and make life easier for your loved ones.

A well-crafted estate plan outlines your financial wishes, protects your assets and ensures your loved ones are financially secure. It can even include guardianship for minor children and pets.

What Is Included in My Estate?

Your estate includes everything you own. Assets typically included in an estate are:

- Property

- Investments

- Pensions/retirement accounts

- Cash, bank accounts or bonds

- Other assets, such as jewellery, art, vehicles and collectables

The Benefits of Estate Planning

A common misconception is that estate planning is only for the wealthy. In reality, having a wealth transfer planning strategy can provide significant benefits for nearly everyone.

Anyone with loved ones, property, or assets they wish to pass on should have a plan in place to ensure a smooth transition. Without one, the courts will make those decisions for you.

However, a significant number of people still put their estate plans on the back burner. A report found over half (53%) of UK adults had not informed anyone of their wishes regarding their estate.

Why Estate Planning Is Important

- Family protection: Ensures loved ones have financial security

- Control over your legacy: Decide who inherits what and when

- Tax efficiency: Reduce or avoid inheritance and other estate taxes

- Avoid probate delays: Proper wealth transfer planning can make transferring assets much faster and smoother

- Incapacity planning: Appoint someone to make decisions if you are unable to

Read more: What Are the Benefits of Estate Planning?

Key Components of an Estate Plan

There is no one-size-fits-all estate plan. It is a process that often includes several essential documents and tools designed to protect your interests and those of your family.

Some of the core elements of an estate plan include:

Trusts

Trusts help manage, protect and distribute your assets efficiently and are often used as a tool to avoid probate. Trusts are frequently incorporated into wealth transfer planning strategies as they can help you reduce your taxable estate.

Most trusts fall into one of two categories — revocable and irrevocable trusts. A revocable trust allows you to change the trust while you are alive, while an irrevocable trust does not.

There are several different types of trusts. Some of these include:

- Bare trusts: The designated beneficiaries have access to the assets in the trust once they reach a specified age

- Discretionary trusts: Trustees have full discretion over how to distribute income and capital

- Interest in possession trust: The beneficiary has access to income from the trust but not the assets that generate the income

- Avoid probate delays: Proper wealth transfer planning can make transferring assets much faster and smoother

- Mixed trusts: Combine elements of various kinds of trusts

Related article: Complete Guide to Estate Planning Trusts.

Will

A will is different to a trust and is one of the most common estate planning documents that outlines your final wishes. For example, how assets should be distributed and who will be responsible for caring for your children.

Power of Attorney

Power of attorney (POA) is legal documentation that appoints someone to handle financial/legal decisions if you’re incapacitated.

There are three main types of POA. They are:

- Financial power of attorney: those responsible for financial decisions

- Medical power of attorney: those responsible for healthcare decisions and other medical decisions

- Durable power of attorney: grants broad authority to make financial, medical and legal decisions

Life Insurance

Life insurance is a key component of legacy planning. A policy offers financial security for your loved ones when you are gone.

There are two common types of life insurance:

- Whole of life insurance: provides cover for your entire life and pays a guaranteed lump sum.

- Term life insurance: provides cover for a specific period, known as a term. A death benefit is paid out if you die within this term.

- An attractive option for high-net-worth individuals (HNWIs) is indexed universal life (IUL) insurance.

IUL insurance offers more flexibility than other products on the market and provides lifetime coverage. It combines a death benefit with a cash value component.

The cash value portion of the policy has growth potential as it is invested in a major stock market index, such as the S&P 500.

Healthcare Directive

A healthcare directive is another legal document that details your medical care preferences.

Ready to speak to a specialist?

Start your journey with Holborn Assets

How Does Estate Planning Work?

Estate planning can be complex, but getting started doesn’t have to be overwhelming.

Essential Steps to Create Your Estate Plan

Creating a wealth transfer plan is a multi-step process. This simple checklist helps ensure you've covered the essentials and are on the right track.

- Make an inventory of your assets and liabilities

- Decide who gets what (beneficiaries) after your death

- Draft your will and/or set up trusts

- Appoint executors, guardians and trustees

- Create a power of attorney

- Review your plan every 2–3 years or after major life changes

To learn how you can get started, read our Estate Planning Checklist Guide.

Estate Planning for Tax Efficiency

Estate taxes, such as inheritance tax (IHT), can significantly reduce the value of your estate. Fortunately, there are strategies you can use to lower the tax burden on your heirs:

- Gifting: Giving a gift to friends and family while you are alive. There is an annual limit to how much you can give away each tax year. Be aware that a gift tax applies to gifts made three to seven years before you die.

- Trusts: Putting assets in a trust can help distribute wealth strategically. Assets in a trust may not count as part of your estate when you die. This can help lower your estate tax bill.

- Exemptions: Assets left to a spouse or charity are exempt from Inheritance Tax (IHT).

Tax rules vary based on your location and asset size, so it is important to work with a professional.

Learn more: Ultimate Guide to Estate Tax Planning.

Download our free guide to UK Inheritance Tax

Learn the ins and outs of Inheritance Tax in the UK to better understand how to maximise the amount of flexibility and control you’ll have

Specialised Estate Planning

Your wealth transfer plan should reflect your situation and goals. When planning their estates, wealthy individuals and expatriates often require a tailored plan that reflects their unique situation.

Estate Planning for High-Net-Worth Individuals (HNWIs)

Estate planning for high-net-worth individuals (HNWIs) can be more complex.

HNWIs have different goals and face additional challenges when planning their legacy. For this reason, a wealth transfer strategy for HNWIs requires a specialised approach to meet those goals and overcome the obstacles.

Some points for HNWIs to consider are:

- Inheritance tax (IHT) liability

- Asset protection strategies for large estates

- Succession planning for business owners

- International assets and tax residency status

Read more: Estate Planning for High-Net-Worth Individuals.

Estate Planning for Expats

Cross-border estate planning addresses the unique challenges that expats often face, such as varying inheritance laws, tax rules, and residency requirements.

For example, UK expats need to verify whether their will is valid overseas, especially if they have assets in multiple countries. The rules differ from country to country, and local laws may not recognise a UK will.

Some points for expats to consider are:

- Residency status and its impact on tax

- Having dual wills (one for each country)

- How assets are treated in each jurisdiction

- Currency and conversion issues

To learn more, read our guide to International Estate Planning for Expats.

How Much Does Estate Planning Cost?

The cost of an estate plan can vary. And while you can take a do-it-yourself approach to estate planning, expert guidance offers peace of mind—especially for complex estates.

What Affects the Cost of Estate Planning?

- The type of services you need

- Estate planning attorney fees

- The complexity of your estate

- Number and type of estate planning documents needed (wills, trusts, etc.)

It's essential to understand the costs upfront based on your situation and needs. That way, you avoid any surprise fees later down the line.

Read our blog to learn more: How Much Does Estate Planning Cost?

Common Estate Planning Mistakes

Even a well-intentioned estate plan can go wrong if certain details are overlooked. But if you know what to look out for, you can avoid some of the common pitfalls.

Top Estate Planning Mistakes

- Failing to plan: This might sound obvious, but sitting down and putting together an estate plan is something most of us tend to put off.

- Not updating a plan: Your estate plan should be reviewed and reflect any life changes.

- Overlooking digital assets: While often overlooked, it is essential to consider your digital assets as part of your estate planning strategy.

- Ignoring tax planning: Tax planning is crucial as it allows you to pass on more to your loved ones.

Read the full list and learn more: 7 Common Estate Planning Mistakes and How to Avoid Them.

Do You Need Professional Help?

While DIY estate planning is an option, professional guidance is essential if you:

- Have significant assets

- Own real estate or assets abroad

- Want to reduce estate taxes

- Want to avoid future legal complications

A qualified financial planner can help simplify an otherwise complex process and ensure everything is compliant and well-structured. As a result, you will have peace of mind knowing your affairs are in order.

Estate Planning Summary

Estate planning is one of those things we often put off. Research found that only 28% of UK adults have a will, with nearly a fifth thinking they do not need one.

Acting now can help ensure that your final wishes are honoured and that your loved ones have financial security.

The earlier you start, the more control you will have over the outcome. Whether you begin with a basic will or engage a full team of professionals, the important thing is to start.

Holborn Assets is a leading award-winning financial services provider. Alongside our legal partners, we provide a comprehensive range of estate planning services tailored to your specific needs and goals.

Be prepared for whatever tomorrow brings. Book a free, no-obligation meeting and learn how we can help you.

To learn more about Holborn and why clients from around the world choose us, download our free brochure.

Your questions, answered

Estate planning is the process of deciding how your assets will be managed and distributed after your death.

An estate plan can:

- Ensure your wishes are followed

- Provide financial security for your loved ones

- Reduce estate taxes

- Simplify or avoid probate

Without a plan, the law decides how your estate is divided, which may not align with your intentions.

Yes. Having a will is not just for the wealthy; it is essential for everyone.

A will gives you control and allows you to:

- Appoint guardians for children

- Designate who inherits personal items or property

- Avoid family disputes

Even a modest estate can become complicated without a will in place.

If you die without an estate plan, known as dying intestate, the law decides who gets what.

This can lead to:

- Long probate delays

- Higher legal fees

- Assets going to unintended beneficiaries

Not having a plan in place can also lead to emotional stress and sometimes conflict for your loved ones.

The earlier you start, the better. Planning your estate sooner rather than later is always the best option, especially if you have dependents or family members who rely on you financially. Life is unpredictable, so early planning protects you and your family in case the unexpected happens.

In general, you should review your estate plan every 3-5 years or after major life events, such as:

- Marriage or divorce

- The birth of a child or grandchild

- Significant financial changes

Those with complex financial situations may want to review their estate plan more frequently.

Yes. Having an estate plan can significantly speed up the probate process or help avoid it altogether. In particular, trusts can help distribute your assets without the need for probate. Avoiding probate not only speeds up distribution but also keeps your affairs private.

Read more about Estate Planning

Comprehensive Guide to Estate Planning for Business Owners

Business owners can lower estate taxes by:

How to Get Started: Estate Planning Checklist

Estate planning might not be exciting, and many people put it off. Still, it is...

A Guide to Estate Planning for High-Net-Worth Individuals

Wealthy individuals can reduce estate and inheritance taxes through strategies...

Read more about Estate Planning

Comprehensive Guide to Estate Planning for Business Owners

Business owners can lower estate taxes by:

How to Get Started: Estate Planning Checklist

Estate planning might not be exciting, and many people put it off. Still, it is...

A Guide to Estate Planning for High-Net-Worth Individuals

Wealthy individuals can reduce estate and inheritance taxes through strategies...

Estate Tax Planning Guide: How to Reduce Estate Taxes

Estate tax planning is important for protecting your wealth and making sure it...

Complete Guide to Estate Planning Trusts

There is an extensive list of assets that you can add to a trust, depending on...

A Guide to International Estate Planning for Expats

Estate planning is vital for anyone looking to secure their legacy and protect...

Comprehensive Guide to Estate Planning for Business Owners

Business owners can lower estate taxes by:

How to Get Started: Estate Planning Checklist

Estate planning might not be exciting, and many people put it off. Still, it is...

A Guide to Estate Planning for High-Net-Worth Individuals

Wealthy individuals can reduce estate and inheritance taxes through strategies...

Estate Tax Planning Guide: How to Reduce Estate Taxes

Estate tax planning is important for protecting your wealth and making sure it...

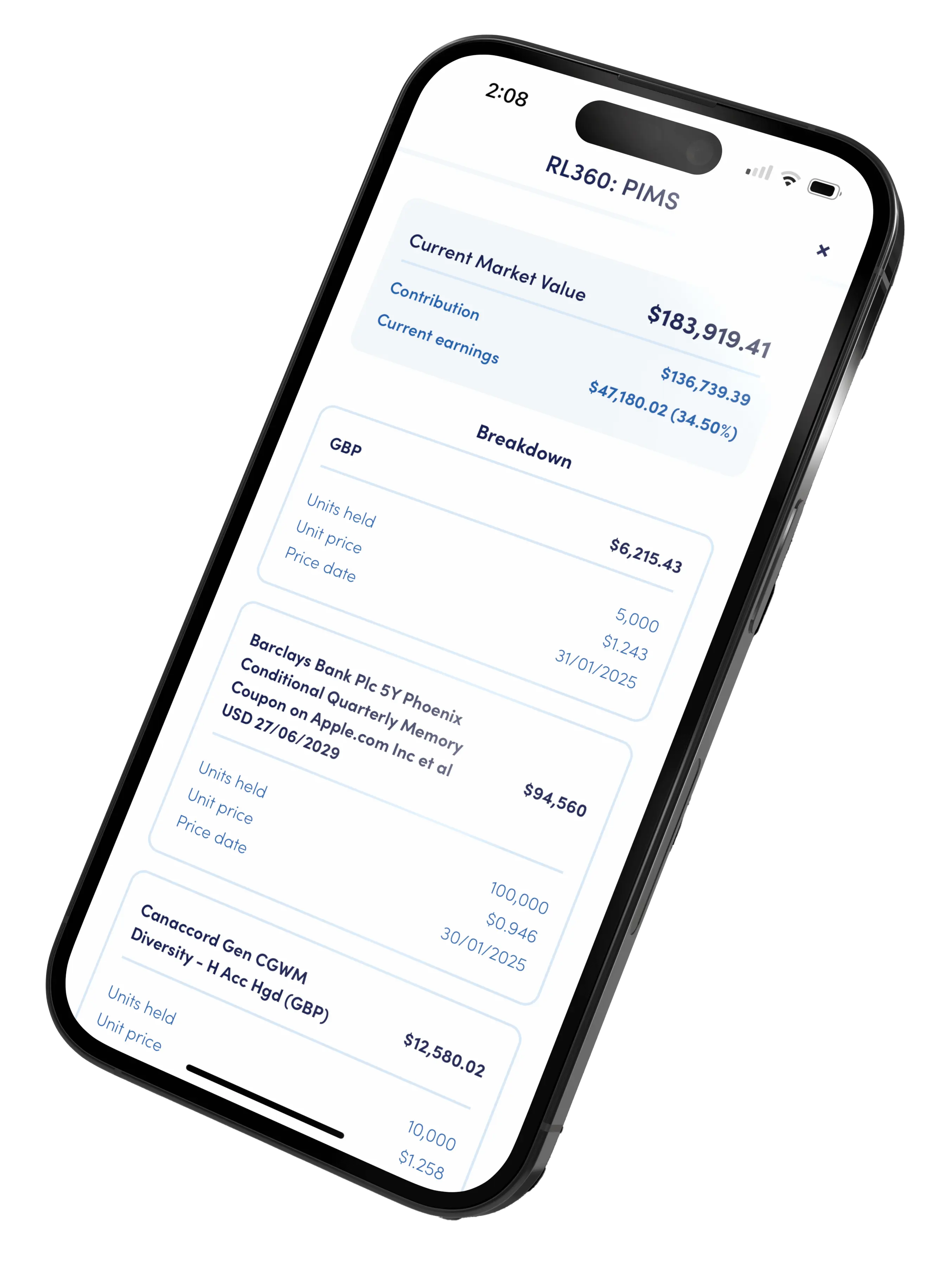

Manage your legacy with the Holborn app

Securely store and manage key legal documents like wills and trust deeds.

Access your portfolio, track assets, and ensure your estate plan is always accessible and up-to-date, wherever you are in the world.