Investment decisions should be made using analysis, logic and rational thinking.

But are they?

One school of thought suggests your financial decisions may not be as rational as you think.

That’s because, as humans, we tend to make decisions based on emotions rather than logic.

In this article, we explore behavioural finance and how understanding it can help you make better investment decisions.

Are we our own greatest enemy?

Before diving into the topic of behavioural finance, we first need to look at the real costs of our choices.

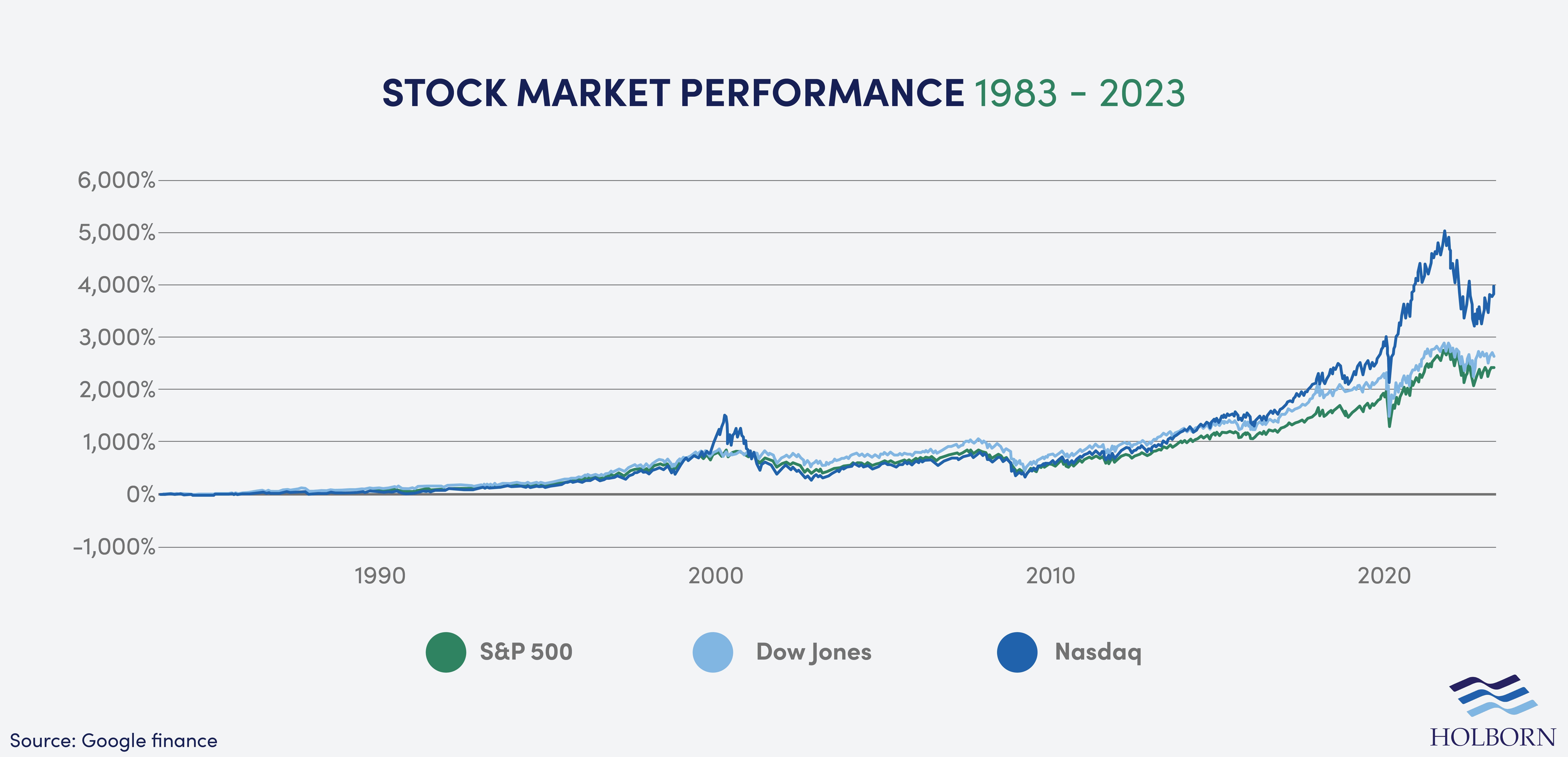

Historically, stock markets around the world have trended up, as shown in the charts below.

As you can see, there have been dips. Yet, generally speaking, the data suggests one thing.

If you invest in a diverse portfolio and leave it alone, you will earn a lot of money. But this isn’t always the case.

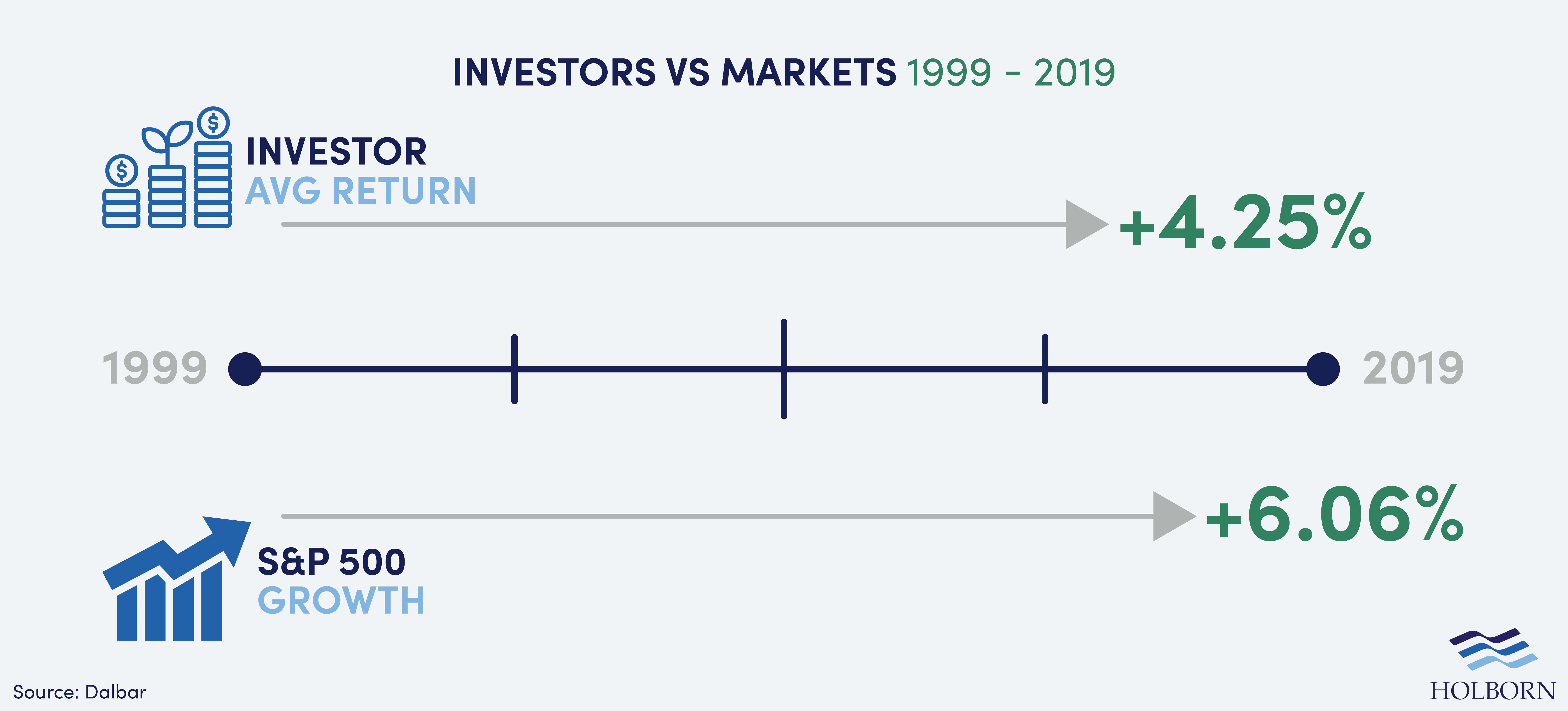

We can go even further to illustrate this point.

Research by Dalbar focused on comparing the rate of return against the performance of a given market.

They found that in the 20 years up to 31 December 2019, equities investors saw an average annual return of 4.25%. However, the S&P 500 index had increased by 6.06% during the same period.

Of course, there are other factors to consider. But it does beg the question; are we our own greatest enemy when it comes to being successful in the markets? Maybe.

But it might not be entirely our fault. The way our brains are wired could be our biggest obstacle to wealth.

Behavioural finance helps us better understand why we make certain decisions and could provide the tools we need to be more successful investors.

What is behavioural finance?

Behavioural finance theory is the study of how psychological and emotional factors influence our decision-making.

Traditional finance theory is based on the concept that investors are rational. They are not clouded by cognitive errors and use the relevant data to make informed decisions.

The approach of behavioural finance is very much the opposite.

It suggests that, as humans, we have inherent flaws. We don’t always act rationally, and we have limits to our self-control. Instead, emotions, cognitive errors and biases can often influence our choices.

In the 1970s, research carried out by psychologists Daniel Kahneman and Amos Tversky found that we often make investment choices using heuristics.

Heuristics are basically mental shortcuts used to make decisions. These shortcuts are usually not the most optimal way of making crucial choices when putting money into the market.

However, one of the main concepts that underpin the field of study is biases and how they influence our choices.

Behavioural finance concepts and biases

In behavioural finance theory, concepts and biases are the things that affect our decision-making, and they can play a major role in outcomes.

Let’s take a closer look at some of the common concepts and biases.

Herd mentality

People have a tendency to follow the crowd, even if it goes against their better judgment. This is called herd mentality, or herding, and it’s not always a bad thing.

Herding saw a large number of less experienced investors jump on the bandwagon and invest in Gamestop, making a lot of money in the process.

However, herd mentality can also lead to market bubbles, crashes and losses for the investor. A prime example of this is the dot-com bubble in the late 1990s.

Mental accounting

Mental accounting is a concept introduced by economist and Nobel Prize winner Richard Thaler.

The concept suggests that we do not treat money as fungible or interchangeable.

Instead, the theory proposes that we mentally sort money into different ‘accounts’. In other words, while the value of money is objective, when we spend it, we treat its value as subjective depending on its source.

For example, let’s say you got an unexpected tax return of $5,000. Spending that money over $5,000 from your personal account would be easier. This is because the value you mentally attach to the money from a tax return versus the money you worked for is different, even if the amount is the same.

Placing different values on money can lead to irrational spending. In the world of investing, you often hear the phrase, ‘only invest what you can afford to lose’.

So when investors get positive returns from a speculative investment, it’s easy to view that as ‘free money’ or ‘money you can afford to lose’.

But remember, all money is equal. It should be treated no differently than the money you have put by in an emergency fund or savings account.

Emotional gap

Our emotions can sometimes cloud our better judgement.

The emotional gap refers to decisions we make based on extreme emotions such as fear and anxiety. This is one of the primary reasons for investors making irrational choices.

Overconfidence

In relation to behavioural finance, overconfidence means thinking we know more than we actually do. This can cause us to overlook crucial information and make less-informed decisions.

This could lead investors to make poor decisions, take on too much risk and lead to financial losses.

Anchoring

Anchoring refers to our tendency to rely too heavily on pre-existing or initial information. In other words, we can become ‘anchored’ to a fixed reference point and use that to judge value and worth.

Here is an example to illustrate the point.

Let’s say you want to know how much financial advice will cost. You speak with one financial adviser, and they tell you their services will cost $10,000. You talk to a second who is just as qualified and experienced. The only difference is they are charging $2,000.

You will naturally go with the second adviser as they seem much cheaper. However, if you had only met with the second adviser and been quoted $2,000, you may not view that as cheap.

That is because, in this scenario, the $10,000 quote was the anchor, and that is what influenced with opinion.

When it comes to investing, anchoring can present a few problems.

It can cause investors to make poor choices. For example, an investor may hold onto an asset that has dropped in value because they have anchored themselves to the original price.

Holding an investment and hoping it returns to the price you paid for it can lead to greater risk.

Confirmation bias

As the name suggests, confirmation bias is when we seek information confirming our beliefs. Sometimes this can lead to us even going against what we believe to be true.

For investors, this could prove very problematic. It can result in missed opportunities or, worse, poor investment choices.

Let’s say you are set on investing in a specific company. There may be one report out there that backs up your beliefs that investing in that company is a sound choice. Meanwhile, there could be multiple reports that go against your beliefs.

By only reading the report that backs up your reinforces your views, you could lose money on a bad decision.

Loss aversion

Loss aversion refers to the tendency for people to be more focused on avoiding risks than making a return on their investments.

An example would be if an investor is more concerned with not losing $5,000 on an investment than they are with a $10,000 gain.

Loss aversion is also tied to the disposition effect. This is when an investor holds on to poor-performing investments for too long, hoping they will recover. On the other end of the scale, it can also result in investors being too hasty and selling winning stocks too soon.

Why behavioural finance is important

The choices we make can have a major impact on our investment outcomes.

But there is a key takeaway here, and that is the importance of self-awareness.

Behavioural finance simply provides us with a blueprint. It gives us an insight and understanding of human behaviour. It also helps us better understand the psychological and emotional factors that can impact our choices.

And by understanding and being aware of our own biases, we become better equipped to make rational choices – Choices that are routed in logic rather than influenced by emotions or cognitive biases.

The role of financial advisers

Financial advisers are experts in their field and can play a crucial role in helping investors avoid some of the behavioural finance pitfalls we’ve highlighted in this article.

Another benefit of working with a financial adviser is to gain a more balanced perspective. Doing so can allow investors to avoid some of the common biases.

That is one of the reasons why a financial second opinion is valuable.

It helps give you the clarity you need to make more informed decisions and develop a long-term investment plan that aligns with your objectives.

Avoid costly mistakes and make sure you are on track to reach your financial goals by speaking to Holborn Assets.

Book a free, no-obligation meeting and learn how we can help you.

All information contained in this article was correct at the time of publication. This article is for informational purposes only and is not financial advice. For personal financial advice, always speak to a regulated professional.

Don’t just take our word for it...

We’re rated ‘Excellent’ on Trustpilot, based on thousands of verified reviews from real client experiences