You’ve saved money, built an investment portfolio, and maybe have equity in a business or property. Now you might be asking yourself if it’s time to get some help managing it all.

If this sounds familiar, you’ve probably already searched online for “do I need a wealth manager” or something like it. It’s a great question, and the answer isn’t always straightforward.

The truth is, most wealth managers have minimum net worth requirements, and these can vary a lot. Let’s look at the numbers, common thresholds, and when professional help can start to make a difference.

Quick answer: at what net worth do you need a wealth manager?

Most firms require between £100,000 and £500,000 in investable assets, rising to £1–5 million for high-net-worth services and £10 million or more at private banks. There’s no single number, though—your financial situation’s complexity matters too.

Net worth vs investable assets: an important distinction

Many people overlook an important detail: the difference between net worth and investable assets.

Wealth management firms with minimum requirements usually focus on investable assets like cash, stocks, bonds, ISAs, and retirement accounts. They often don’t count your total net worth, which might include your home or art collections.

For example, if your net worth is £1.5 million and it includes an £800,000 home, a wealth manager might see you as a £700,000 client rather than a £1.5 million client.

Here is a general guide showing the standard wealth classifications.

In the end, it’s not about how much money you need for a wealth manager, but how much you have in investable assets.

How much money do I need for a wealth manager?

Many wealth managers require clients to meet a certain investable asset minimum before working with them. The latest World Wealth Report found that 97% of firms still group clients by wealth bands.

In the UK, the minimum amount to access wealth management services typically ranges from £100,000 to £500,000 in investable assets. However, many advisers also serve the ‘mass affluent’ market — those with at least £50,000 in investable assets.

These numbers are just general guidelines. Some firms don’t have a set minimum, while others focus on specific groups, such as business owners or expatriates, rather than requiring a specific level of wealth.

Qualifying for wealth management is one thing, but when does the cost of hiring a wealth manager become a good return on investment?

At what net worth does wealth management become worthwhile?

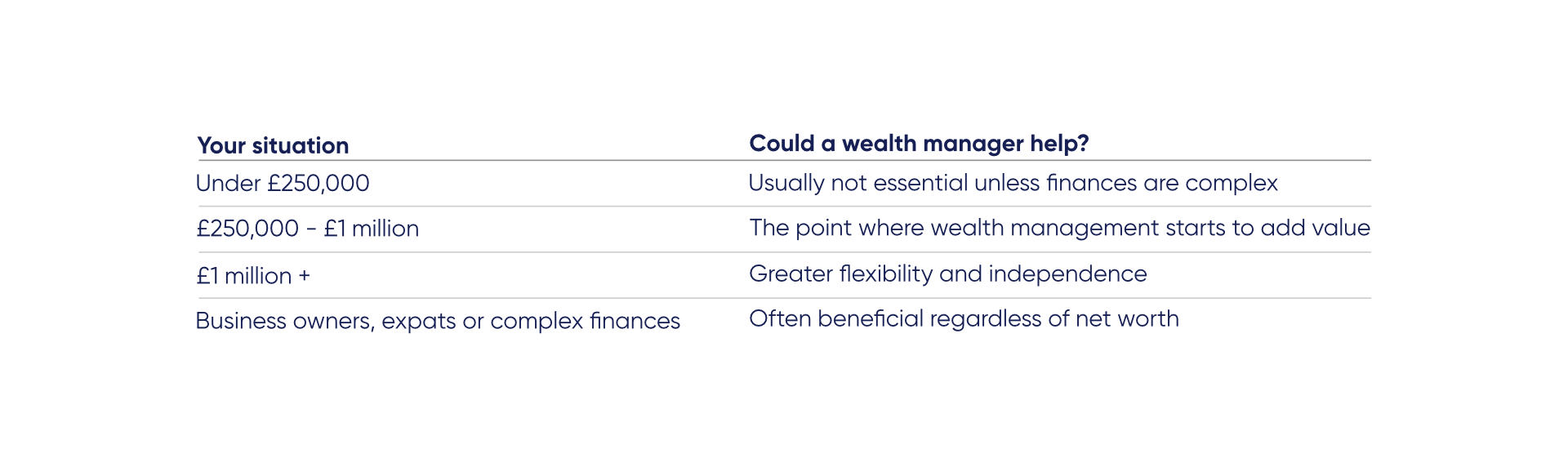

Most wealth managers say their services start to add real value at around £250,000. The actual benefit depends on your goals and other factors, but there are common points where professional help becomes more valuable.

Under £250,000

At this stage, you’re still building your wealth. Wealth management might work with you, but financial advice could be a better fit for your needs.

However, if you've recently inherited money or have complicated financial affairs, working with a wealth manager may still be worthwhile.

£250,000 to £1 million

This is when a wealth manager can really start to help. Tax planning, investment diversification, and retirement planning all have a bigger impact on your long-term results.

Above £1 million

When your assets go over £1 million, you’re usually considered a high-net-worth individual. At this point, protecting your wealth becomes as important as growing it. Many see this as the point where wealth management becomes essential, not just helpful.

Why £1 million is the common benchmark

The term ‘high-net-worth individual’ is often associated with wealth management.

High-net-worth individuals (HNWIs) usually have at least £1 million in investable assets. This is the point at which clients typically need professional advice on investments, taxes, and estate planning. Bundling these services to support someone across several areas of their financial life is what sets wealth management and financial advice apart.

Above this level are ultra-high-net-worth individuals (UHNWIs), with £30 million or more in investable assets. Like HNWIs, they need professional advice, but private banks and custom services also become important.

When weighing whether you need a wealth manager, your asset levels are important, but they don't tell the whole story.

It’s about more than a number

In many cases, financial complexity—not net worth—is the strongest indicator that professional advice could add value.

People with much less than £1 million can still benefit from professional help if their finances are complicated. The better question is whether your financial situation has become complex enough.

You may benefit from wealth management if you:

Own a business

Have international assets

Live or work overseas

Have inherited significant assets

Are planning retirement

Want to pass wealth to future generations

One group that can benefit from wealth management is expats, regardless of wealth. Living and working overseas often leads to a complex financial situation, especially when dealing with taxes and cross-border planning.

The benefits of working with a wealth manager for HNWIs

Usually, the more wealth you have, the harder it is to manage. That’s why high-net-worth individuals can really benefit from a dedicated wealth manager’s expertise.

Key benefits of wealth management for high-net-worth individuals include:

Personalised investment strategy:

Portfolios are built around your goals, risk tolerance, and time horizon, rather than relying on generic products.

Tax efficiency:

Structuring investments and income to legally minimise tax liability and preserve more wealth.

Estate and succession planning:

Ensuring assets transfer smoothly to heirs while reducing inheritance tax and probate complications.

Risk management:

Diversification and hedging strategies that protect wealth against market volatility and unforeseen events.

Consolidated financial oversight:

A single coordinated service that supports you across all areas of your financial life.

But what if your finances aren’t complicated enough for a wealth manager, yet you still want professional advice? There’s another option.

Wealth management vs financial advice

Two terms that are often used interchangeably are financial advice and wealth management. They’re closely related, but not the same. The right choice often depends more on the kind of support you need than on your wealth.

A financial adviser usually focuses on specific goals. They can offer advice on investments, pensions, insurance and other financial products.

Wealth managers are a type of financial adviser who usually work with high-net-worth or ultra-high-net-worth clients. They cover many parts of your financial life, not just one area. Their service is broader and ongoing, combining investment management, financial planning, tax efficiency, estate planning, and wealth preservation.

Both financial advisers and wealth managers offer value, but they fit different goals and needs.

Weighing up the costs

Wealth management fees depend on factors such as the provider and the level of service you choose.

Common pricing models used by wealth managers are:

Assets under management (AUM):

A set percentage of the value of the assets being managed.

Fixed fees:

A flat fee charged monthly, yearly, or for a specific project.

Hourly rates:

A set hourly consultation fee based on the time spent giving advice or handling your account.

It’s important to understand the fee structure before you start. Also think about the range of services, the provider’s experience, their investment approach, and the value of ongoing advice.

Summary: is a wealth manager worth it for you?

Many people assume wealth managers are hired solely to generate higher investment returns. In reality, their value often extends much further.

If you have relatively straightforward finances or a smaller portfolio, financial advice may be sufficient. But as wealth and financial complexity increase, comprehensive wealth management can provide significant long-term value.

In the end, the best time to think about wealth management is when expert advice could improve your financial results, not just when you hit a certain net worth.

All information contained in this article was correct at the time of publication. This article is for informational purposes only and is not financial advice. For personal financial advice, always speak to a regulated professional.

Don’t just take our word for it...

We’re rated ‘Excellent’ on Trustpilot, based on thousands of verified reviews from real client experiences